We believe you can go further and do more when you have a trusted risk-discussion partner on your team, who will look at your business holistically to uncover new opportunities.

We are a leading global reinsurer that helps insurance companies reduce their earnings volatility, strengthen their capital and grow their businesses through reinsurance solutions.

The issue. Individual life insurance sales typically involve a lengthy application process, including multiple face-to-face interactions and appointments for medical testing. This process is increasingly unaligned with modern customer sales expectations and is made all the more unacceptable and impractical in the current COVID-19 environment (social distancing).

The solution? Many Life & Health insurers across the Asia-Pacific region are adding online digital sales capabilities. These are structured to simplify the sales process for the applicant and remove the need for face-to-face contact.

However,… Results have not been as good as hoped, and many consider that the previous status-quo of doing business will return once COVID-19 has passed – the problem being that the historical issues that the industry has struggled with remain, including:

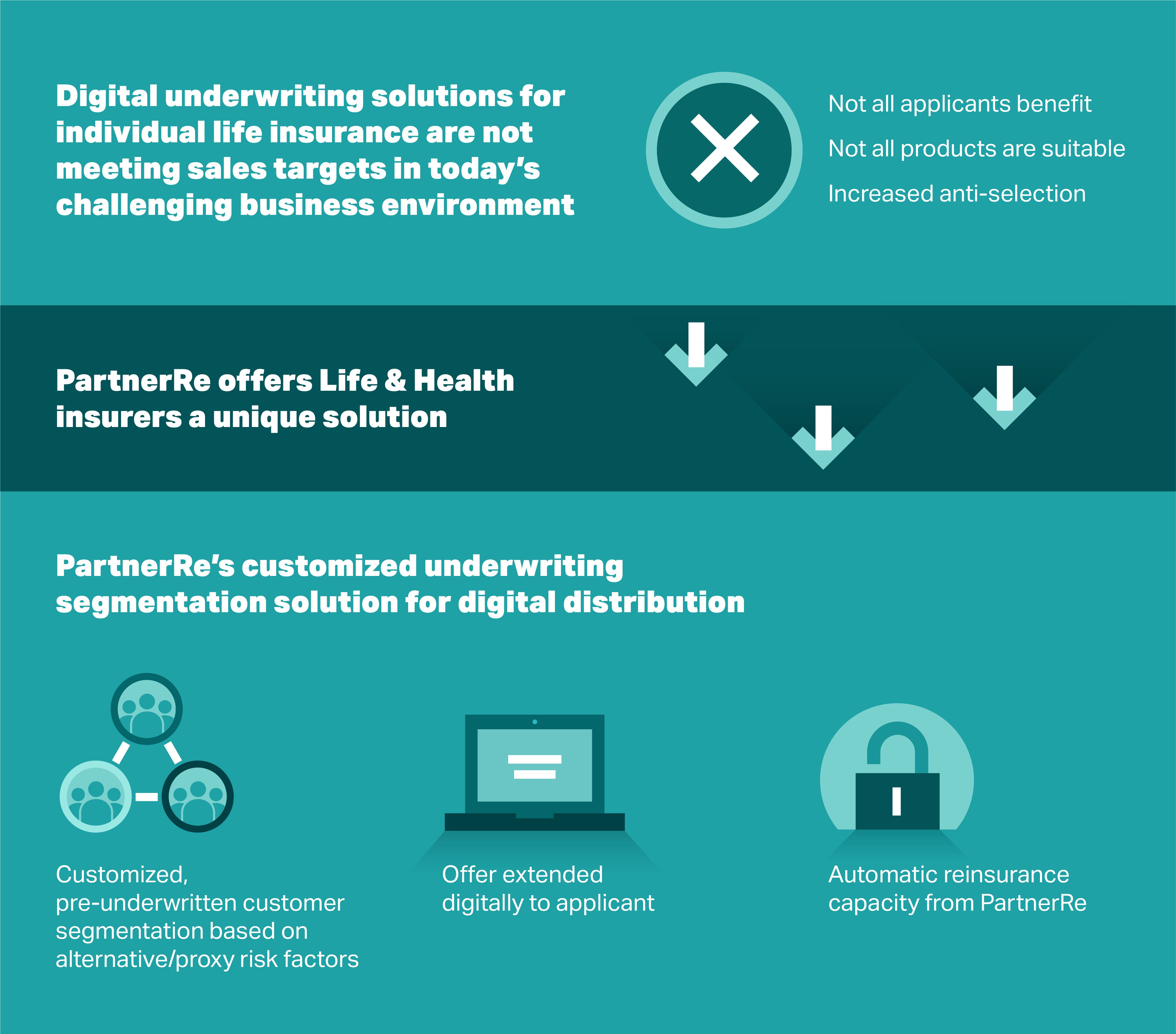

Not everyone benefits. For many applicants (e.g. those with previous conditions), medical testing and lengthy underwriting are still required.

Not all products are suitable. By simplifying the sales process, the necessary ‘push’ element of some individual life insurance cover types is removed.

Anti-selection is increased. Online solutions come with a pricing load that makes them less competitive for individuals representing better risks. This results in anti-selection, an effect compounded by ageing populations.

An alternative solution. PartnerRe can offer an alternative, unique solution to the environmental and competitive evolutions facing Life & Health insurers – a solution that captures the current momentum behind digital channels and propositions, whilst overcoming the above-mentioned issues.

PartnerRe’s customized underwriting segmentation solution for digital distributions

This solution combines a customized, pre-underwritten customer segmentation approach based on alternative/proxy risk factors, with a product offer extended digitally to the customer and automatic reinsurance capacity.

Our innovative and easy-to-implement underwriting solution for defined, distribution-led customer segments will help you navigate COVID-19, grow your life portfolio and stay aligned to customer expectations in a digital world.”

Underwriting customer segments using alternative/proxy risk factors, without scoring models or requirements for big data

As US Life Scoring Models have already established, there is a significant correlation between mortality and non-traditional individual risk factors such as credit score, driving records and drug purchase behaviour. This offers an alternative, potentially less complex route to pricing and selecting insured lives.

Without the standardized mortality proxies of the US or the data of big tech players (potential new competition for insurers), for the Asia-Pacific region, our life underwriting and propositions team have developed a proxy, non- (traditional medical underwriting) data driven, simplified underwriting solution based on distribution-led existing customer segmentation (e.g. data linked to wealth, income and occupation). This allows for pre-selection and proxy-underwriting of (better) lives, hence enabling a simplified and seamless digital application process.

This solution combines a customized, pre-underwritten customer segmentation approach based on alternative/proxy risk factors, with a product offer extended digitally to the customer and automatic reinsurance capacity.”

This also looks to solve the aforementioned historical issues of traditional digital propositions: Customers are now pre-underwritten and thus avoid the need for lengthy medical testing and underwriting, the products are pre-selected for those distribution-led segments, and anti-selection is reduced as the risk is well defined.

Examples of customer segments that we have created segmented underwriting solutions for:

Premium bank customers

Salaried customers

Individual credit life customers

SME credit customers

Business sourced by agents (differentiated on the basis of agent attributes)

Our clients can choose which of our pre-selected available segments best fits their market and needs.

We follow a client-up – rather than the more usual ‘prescriptive’ – approach. We begin with conversations with the distribution teams or partners of our client to understand the root causes of sales issues, and then tailor the solution accordingly.

Over time, this solution has the added benefit of accumulating quality proxy underwriting data that can used by our data analytics team to run ever-more advanced models and open-up new possibilities for our clients for new segmentations.

Expert underwriting

An extension to this solution is the addition of PartnerRe’s expert, cloud-based, easily implemented underwriting system. The system can be easily and quickly installed at multiple points of sale, depending on your need.

Contributors

Bryce Shepherd, Head of Strategy, Life & Health, Asia Pacific

Sohila Kwan, Head of Business Development, Life & Health, Asia Pacific

Contact Us

Contact us and we can work with you to investigate how this solution could help you maintain and grow your portfolio by improving your customer sales experience for selected segments and countering the business challenges posed by COVID-19. We look forward to talking to you soon!

This article is for general information, education and discussion purposes only. It does not constitute legal or professional advice of PartnerRe or its affiliates.